|

Hindsight is 20/20” — it’s a cliche adage, but it’s pretty accurate when it comes to moving! It seems that you always wish you organized differently, planned more, or simply had an easier way to navigate the moving process. Luckily, we’ve got you covered! These 50 hacks are the most comprehensive guide to staying ahead of moving woes.

Before You Move

Via Rent Fluff

Via LifehackerSave Time, Money, and Hassle While Packing

Via Grown and Flown

Via Listotic

Via The Life You Live

Via Apartment Therapy

Via Awesome Inventions

Via Awesome Inventions

Via ListoticMoving Day Must-Dos

Via Clutter Interrupted

Article taken from: Updater.com

2 Comments

With millions of moves every year in the United States, it’s a minor miracle that most of them go smoothly, with no issues whatsoever. Hiring quality moves is a must, of course.

But even with so many smooth moves, scams or shoddy practices do occur. It’s in your interest to be informed about every step in the process. Here are 11 ways to hire the right team for your move:

Article taken from : Moving.com The Top Misconceptions About a Power of Attorney Get answers to some of the most frequently asked questions about a POA by learning from these misconceptions:

Misconception #1: You can sign a power of attorney if you are legally incompetent.Someone cannot appoint a power of attorney (or sign any legal document) if they are incapacitated. According to Furman, this is one of the most common misconceptions about the power of attorney. “So many times I get a phone call from someone who says ‘I just got certification from my dad’s doctor to state that he is not competent so I can have you do a power of attorney and living trust for him,’” he says. Contrary to popular belief, only a mentally competent individual can appoint a POA for themselves. However, because this misconception is so wide-spread, Furman wrote about it in detail in “The ElderCare Ready Book.” In Chapter 10, “Famous Last Words,” Furman writes: “For some reason, people do not grasp the concept that one needs to be competent to execute legal documents. I understand that people generally look at what they need to get accomplished first; for example, accessing a bank account because dad is not able to anymore. However, at some point, they are told, informed or just believe that dad must have lost their legal capacity prior to the signing of a power of attorney or living trust. This is just backwards! Once Dad lacks legal capacity, then he can no longer sign any legal documents including a power of attorney or living trust, which was intended to be used if Dad became incompetent. The only recourse is then a conservatorship or guardianship proceeding through the court, which is a very costly and time-consuming process.” Misconception #2: You can find a power of attorney document on the internet.Power of attorney forms may be found online, however, it is heavily ill-advised to use. A power of attorney should be created to appropriately represent the specifics of the unique circumstances and the decisions and care that need to be made on behalf of the person. “People should stay away from the internet and have a power of attorney custom drafted to your circumstances,” Furman advises. Getting a power of attorney document from the internet means that you could be paying for a document that::

Misconception #3: A power of attorney grants the agent the right to do what they please with your estate.By law, the agent under a power of attorney has an overriding obligation, commonly known as a fiduciary obligation, to make financial decisions that are in the best interests of the principal (the person who named the agent under the power of attorney). A power of attorney doesn’t grant full financial rights regarding assets. “Based on fiduciary obligations, just because it says you have the power doesn’t mean you have the right,” Furman explains. “The right to act is based on fiduciary circumstances. If the action is not in the best interests of the principal then, notwithstanding that you have the power to act, you do not have the right to act,” he says. “It’s important that people understand that this fiduciary obligation is not stated in the power of attorney, and it doesn’t need to be because it is implied by law,” Furman says. “The fiduciary obligation is an aggressive restriction placed on the agent under a power of attorney” to protect the principal. People hesitate towards getting a power of attorney because they are worried that the agent will mismanage their affairs and assets. Legally, your agent shouldn’t do something that is not in your best interests — that is their fiduciary obligation to you as your agent. However, it can’t be emphasized enough that you must appoint someone you trust. Furman advises that you try to choose someone who is trustworthy and has integrity, especially if their power of attorney is going to extend after you are incapacitated. Misconception #4: There is one standard power of attorney.The principal determines the type of powers to grant their agent in the power of attorney document, which is why it should be drafted by an experienced attorney in the court so that it covers the principal’s unique situation. With that being said, there are types of powers of attorney people frequently about. These include:

A general power of attorney governs all financial powers covered by a power of attorney (like buying or selling a property or otherwise managing one’s assets). However, the specific language of a power granted will depend on the decisions outlined in the signed document. The powers in a POA are specific, especially when custom drafted. The agent needs to check the POA document to see if the necessary authority over the principal’s affairs has been granted. What is a Limited or Special Power of Attorney? A limited or special power of attorney does not have all powers. For example, a power of attorney could be drafted, which only grants the power to conduct a real estate sale for the title of one property. In California’s Probate Code, there are exceptions to the rule about what powers general POA grants. Although this law can vary by state: “In California if certain powers are not expressly written in the general power of attorney then they still don’t exist,” Furman explains. “For example, the power to gift, the power to create a trust on behalf of the principal, the power to disclaim a gift — if these powers are not expressly written in the general power of attorney then they don’t exist — even with a ‘catch-all’ clause in the document, such as a phrase saying ‘all other powers are granted,’ they don’t exist unless they are specifically written in,” he says. A Health Care Advanced Directive (HCAD) allows an agent to manage health or medical decisions for the principal should he or she become incapacitated. This document is meant to give guidance for the principal’s health care (about the principal’s wishes to remain on or off life support among other health-care related situations). A Physician’s Order Regarding Life-Sustaining Treatment (POLST) is not a power of attorney. This document is a directive for doctors and first responders who need to know the principal’s resuscitation wishes in an emergency health situation. What is a Durable Power of Attorney? A durable power of attorney can withstand the mental incapacity of the individual, but not death. A durable POA allows the agent to continue to act on the principal’s behalf, even if the principal is mentally incompetent. This authority is often granted to trusted agents who can manage the duress of end-of-life medical care decisions regarding health, as they may be faced with these important decisions once the principal can no longer express his or her wishes. Occasionally, the court may terminate the durable power of attorney documents in the case of divorce, so there needs to be specific wording in the signed document that clarifies whether the managing of affairs extends in this case. Misconception #5: A General Power of Attorney and Durable Power of Attorney are the Same Thing.All powers of attorney terminate in the event of death. As such, once a person has passed away due to health issues, the authority granted to the agent under the power of attorney terminates. What is the Difference Between Power of Attorney and Durable Power of Attorney? Power of Attorney broadly refers to one’s authority to act and make decisions on behalf of another person in all or specified financial or legal matters. It also refers to the specific form or document that allows one to appoint a person to manage his or her affairs. Durable POA is a specific kind of power of attorney that remains in effect even after the represented party becomes mentally incapacitated. General Power of Attorney vs. Durable Power of Attorney? The key difference between a general POA and a durable POA lies in incapacity. Regular powers of attorney all terminate if the principal dies or becomes incapacitated — meaning that the agent can legally engage in business on behalf of the principal until the principal dies, is mentally incompetent, and/or can no longer make informed decisions independently. Once either of those events occur, the power of attorney is no longer valid. This general power of attorney might be useful if the principal is out of the country or otherwise indisposed, but the durable power of attorney is needed if the principal is no longer capable of making crucial decisions about health care on his or her own. What Does a Durable Power of Attorney Mean? In regard to a durable POA, the word “durable” specifically means that the effectiveness of the assigned power of attorney remains in effect even if the principal becomes mentally incompetent. Typically, there are four situations that would render powers of attorney null and void:

Article Written By: By Kimberly Fowler for aplaceformom.com Many real estate investors know that when they do an exchange, they can’t touch the money, they have to identify what they are going to buy within 45 days, and close on any replacement properties within 180 days of the closing date of the property that is sold. While these facts are true, there are some other things to understand ahead of time that will make it easier to have a smooth and successful 1031 exchange. Here are five points to consider.

1. Sign Exchange Documents Before You Close The 1031 exchange rules allow you to sell your “relinquished” property to someone, and acquire your “replacement” property on a later date from a different person. By signing exchange documents and following the other rules, you can take what would otherwise be a sale followed by a purchase and turn it into an exchange. It’s essential to sign exchange documents on or before the date that you close on the sale of your relinquished property. Exchange documents include an exchange agreement entered into between the real estate investor and the intermediary, an assignment of your rights under the contract to sell the relinquished property and a notice to the buyer of the assignment. On or before the date you close on the purchase, you will also need to sign an assignment of your rights under that contract and you will need to give the seller notice of that assignment. The intermediary assists with this documentation. 2. Think About Who Will Acquire Replacement Property The same taxpayer who sells the relinquished property must buy the replacement property. What if your lender requires you to acquire the replacement property in a single asset entity? This is workable because a single member limited liability company is disregarded for tax purposes. So, for example, an investor can sell his relinquished property that has been held by him individually and can acquire the replacement property in an LLC as long as he is the only member/owner of the LLC. For more information, read our article Vesting and 1031 Exchanges – Same Taxpayer Rule 3. Buy Enough Replacement Property to Defer All of the Gain In order to completely defer all of the tax you would otherwise have to pay on the gain, you must do two things. First, you must acquire replacement property that is equal to or greater in value than the relinquished property. So if you sell something for $1 million, you must acquire replacement property worth at least $1 million or the transaction may be partially taxable. Second, you must invest all of your net equity from the sale into the purchase. If you sell something for $1 million that has a $300,000 loan on it, you must invest the full $700,000 you net out of the sale into the replacement property in order to completely defer the taxes. (This example ignores expenses to keep it simple.) To summarize, in this example, you would need to acquire replacement property for at least $1 million, invest $700,000 of cash into it, and then either borrow $300,000 or invest your own funds in that amount. For more information, read our article Financial Requirements in Structuring a Fully Deferred Exchange 4. Think About Expenses There are some expenses that can be paid with the exchange proceeds that will not cause the deal to be partially taxable. For example, brokerage commissions, escrow fees, exchange fees and transfer taxes are generally considered to be this type of expense. On the other hand, when you are selling the relinquished property, if you give the buyer a credit for security deposits or pre-paid rents, you are using exchange proceeds for non-exchange expenses and it could result in your exchange being partially taxable. For that reason, it’s best to come in with your own funds to pay these if you don’t want to pay any tax. For more information, read our article Closing Costs in a 1031 Exchange – a Trap for the Unwary? 5. Think About Experience and Safety Your intermediary will provide vital guidance through the 1031 exchange process. You may need special expertise when dealing with seller financing, reverse and build to suit exchanges, dissolving partnerships, and other unique issues that take careful planning and guidance. Additionally, when you do an exchange, your funds are held by the intermediary until you use them to acquire replacement property. It’s important to find out how those funds are held – are they in a separate account identified by the name and tax ID number of the investor? Are they held in an FDIC-insured bank account or invested in securities? Is the intermediary financially strong and reputable? A debt consolidation can help you lower your monthly payment and help improve your credit, but only if you stick to a plan to pay down your debt.If you have high-interest credit card balances on multiple accounts, just making those monthly payments can be so tough that you can’t afford the things you really need or want — much less save any money. It may also stress you out. In this situation, debt consolidation might be a smart decision. But before you get started, let’s dig in to understand how debt consolidation can affect your credit scores.

Ways to consolidate your debtThe basic idea of debt consolidation is to merge multiple credit or loan balances into one new loan. But not all debt consolidations make sense. Here are four ways you can consolidate debt depending on your credit and savings:

It may also simplify your payments. When you have many accounts to manage, you are more likely to make a mistake and miss a payment. Missed and late payments can hurt your credit scores, so consolidating everything into one monthly payment might help protect your credit from a payment mishap. How debt consolidation affects credit scoresWhen you consolidate debt, you pull several levers at once that help or harm your credit. Here are some short-term causes of a credit score drop when consolidating debt:

Bottom lineConsolidating your debt into a new, lower-interest loan — a balance transfer credit card, personal loan or home equity loan — may hurt your credit scores in the short- or medium term. But if you make regular, on-time payments on that consolidation loan and pay it off in a reasonable amount of time, your credit scores should recover and may even improve over the long run as you get rid of debt faster and establish a sound payment history. Article Written By: Eric Rosenberg is a finance, travel and technology writer in Ventura, California. He has an MBA in finance from the University of Denver. When he’s away from the keyboard, Eric enjoys exploring the world, flying small airplanes, discovering new craft beers, and spending time with his wife and daughters. You can connect with him at PersonalProfitability.com or EricRosenberg.com.  Plumbing Leaks: 8 Smart Tips to Stop Them

Plumbing leaks can be prevented with a few simple measures. Plus, learn what to do when leaks occur. Plumbing leaks and the resulting water damage repairs or mold cleanup can be costly. Avoid the inconvenience with some good habits and modest investments in time and money. 1. Locate Your Home’s Main Water Shut-Off Valve If there’s ever a plumbing leak, you can go straight there and quickly turn off the water to the entire house. 2. Install Shut-Off Valves at Individual Appliances and Fixtures This allows you to keep water flowing in other areas of the house while making site-specific repairs. You can find quarter-turn, ball-type shut-off valves for less than $10; you’ll pay around $50 to $150 per hour for plumber, often with a minimum two-hour charge. 3. Install a Flow Sensor Install a flow sensor that detects plumbing leaks and automatically shuts off water to the entire house or a specific appliance. Those devoted to a specific appliance start around $75. Whole-house flow sensors can reach into the thousands. Plus, factor in the cost of a plumber. 4. Remove Hoses from Outdoor Spigots Remove hoses from outdoor spigots in the winter to prevent frozen water from cracking the pipes and causing plumbing leaks, or worse, a flood. Install frost-free hose bibs at exterior spigots. 5. Add Pipe Insulation Add pipe insulation to the plumbing in cold parts of your house—such as garages, basements, and crawl spaces—to avoid frozen pipes (and to shorten the wait for hot water). Pipe insulation tubes cost as little as 35 cents per foot. 6. Don’t Use Exposed Pipes as Hanger Rods for Laundry or to Store Clothes Doing so can loosen joints and fasteners and lead to plumbing leaks. 7. Don’t Overload Vanities and Sink Cabinets When you crowd stuff into your cabinets, you can jostle water supply pipes and drains, loosening connections and causing plumbing leaks. If drips occur, they’re tough to spot amid piles of cleaners and spare TP. 8. Fix Problems Quickly Even small leaks can make pipes corrode more quickly, and cause significant water damage or mold. Take the time to periodically scout for signs of leaks and drips. When you buy a home, it’s normal to worry that something may go wrong. Perhaps you’ll move in only to find that the fridge has gone on the fritz or that your plumbing has turned your basement into a swimming pool. Television ads this time of year offer a way to arm yourself against such calamities: They suggest buying a home warranty.

Such warranties are designed to cover what home insurance policies won’t. They are actually service contracts that promise to pay for the cost of repair or replacement if covered items, such as appliances, plumbing, and heating and air conditioning systems, stop working. To be sure, having a home warranty can provide you with peace of mind if things go wrong. But you should also realize that the providers of these plans have built-in wiggle room that can make it easier for them not to make payments. As a result, consumers have complained to the Better Business Bureau about their warranties, often because they didn’t get the payouts they expected, according to Katherine Hutt, a spokesperson for the Bureau. An alternative to buying a plan could be to self- insure. Consumer Reports has long recommended that consumers put the money they would otherwise spend on a home warranty or a service contract into a savings account dedicated to product repair and replacement. That way, you won't risk paying for a plan that may not provide the coverage you expect. If you're thinking of buying a home warranty instead, your first step should be to evaluate the likelihood that you’ll be able to use it. There are plenty of limitations—they generally don’t cover non-mechanical items such as your windows or the structure of your home. Also, keep in mind that if you’re purchasing a new home, the items inside are probably still covered by the manufacturer's warranty and the builder's warranty, says Edgar Dworsky, a consumer lawyer who runs the website. You have better reason to consider a home warranty if the home and the appliances are older. Questions to Ask Before you buy a home warranty, ask yourself these questions: 1. Do I already have protection? If you paid for your appliances with a credit card, you may be covered, Dworsky says. Some credit cards, like most American Express cards, automatically double the manufacturer's warranty, usually up to 12 months, on items you purchase with the card. Others, such as the Citi Double Cash card, provide an additional 24 months of protection, no matter how long the manufacturer's warranty is. 2. How much will it cost? The answer depends on the kind of plan you buy and the provider you choose. You can generally purchase one of three kinds of plans: a home warranty for one particular appliance, for all your appliances, or for your appliances as well as your plumbing and electrical systems. Prices vary depending on the coverage you choose. At American Home Shield, for example, a plan that covers most major appliances costs $200 annually, and one that also includes your home’s electrical and plumbing systems costs more than $800. Besides the cost of the plan, there are likely to be additional expenses. When things go wrong, you’ll also have to make a co-payment when a contractor comes in to do the work. Fees range from around $60 to $125, depending on the work that needs to be done, according to the plans we examined. 3. Am I clear about what the warranty covers? Hutt from the Better Business Bureau says that most of the complaints the Bureau receives are because consumers don't understand the coverage their plans provide. The takeaway: Be sure to read the terms and conditions carefully. When we examined home warranty plans, we found that some policies will cover your refrigerator but not the ice maker that comes with it. Other policies may cover your hot water heater but not the water tank itself. Sometimes, if your appliance breaks under particular circumstances, it won't be covered. An oven, for instance, may not be covered if it stops working while in self-clean mode or if it is damaged by a power surge, according to the plans we examined. How you care for your appliances also matters. If you failed to perform routine maintenance or if an appliance wasn't properly installed, the home warranty provider could argue that it won't pay for repairs. There could even be a pre-existing condition—even if it wasn’t evident to you when you bought the home warranty—that allows the provider to not cover the item. 4. Will a broken item be repaired or replaced? Most home warranties explain that if a repair is considered too expensive, the provider might offer to replace a broken item instead. In such a situation, the home warranty company may give you only the depreciated value, requiring you to pay more to get the same model you had before. 5. Are there limits as to how much a plan will pay out? There are, but it depends on the kind of plan you purchase and the provider. The plan from America's 1st Choice Home Club, for example, pays up to $2,000 over a 12-month membership term to access, diagnose, repair, or replace one covered item. Unless otherwise stated, it will pay a maximum of $10,000 for all covered items.  Credit card utilization, the ratio of what you owe on your credit cards to your credit limit, plays a major role in the calculation of your credit rating. According to FICO(R), the creators and maintainers of the FICO credit score model, it’s 30% of your score. Do a brief Internet search and you will find most experts touting the rule that keeping your credit utilization under 30% will maximize your score. Well, that’s not exactly true.

Why Credit Utilization is so Critical to your Credit Score Being punished for high credit utilization may seem counter-intuitive: why would lenders give you a certain credit limit and then punish you when you try to use it? But that’s exactly what happens. In hard numbers, credit utilization makes up 30% of your credit score. As a comparison: your payment history makes up 35% of your score, the average age of accounts is 15%, the mix of credit is 10% and the amount of new credit that you have is 10%. So why does credit utilization make up so much of your credit score calculation? Higher rates indicate danger: • The bigger your debts, the less likely you will be able to repay them. • Lenders also feel that someone who hits their credit limit each month or even goes over them does not demonstrate financial prudence. • Lenders get nervous when you’ve used your credit limit because if you had the money to pay down your bills, you wouldn’t have to keep borrowing more money.  1. Install a security system.

2. Keep your windows covered of frosted. 3. Upgrade to motion detected lights. 4. Secure the garage door. 5. Don’t leave garage remotes in the car. 6. Use timers.  Invest In a secured credit card from a reputable Credit Union.

What is a secured credit card? It’s a credit card that offers you an opportunity to build or rebuild your credit with responsible use. A secured credit card also requires a refundable security deposit, which is held as collateral for the account. No interest is applied to the security deposit and the deposit is returned when the account is closed.  What is the difference between a short sale, pre-foreclosure, and foreclosure? If you're considering purchasing one of these kinds of properties, it's very important to understand what these terms mean and how the home's status could affect its sale.

The first rule of thumb: Proceed with caution. The pitfalls for the average buyer are numerous when it comes to a short sale or a foreclosure, according to Virginia Field, a Realtor® and instructor for the National Association of Realtor®'s Short Sales and Foreclosure Resource. Let's take a look at these three distinct real estate terms and what they mean for buyers. Short Sale A short sale is when the property owner owes more on the mortgagethan the market value of the property and is asking the bank to accept a short payoff of the loan," explains Cathy Baumbusch, a Realtor in Alexandria, VA. A short sale may or may not be in pre-foreclosure, but the homeowner is asking the bank to let it sell the property for less than what is owed on the loan. Short sales go through a real estate agent, but they don't function exactly like your typical real estate deal. "The biggest misconception the average consumer has about buying a short sale is not realizing how long it takes," says Field. "It can take between six months to a year to close. Also, people think they are going to get a screaming deal, but they have to understand that the bank is going to try to get as much back as it can." Even more frustratingly, a seller can accept an offer on a short sale, but that doesn't guarantee that the deal is going to close. If the lender is not satisfied with the sale price, the home is not going to close. In some cases, foreclosure makes more sense for the lender because there are fewer costs associated with a foreclosure than a short sale. Pre-foreclosure A home is in pre-foreclosure if a homeowner is more than 90 days late on the mortgage payments and the bank has begun the foreclosure process. "A pre-foreclosure is a property in the process of foreclosure but is still legally owned by the owner. It may or may not be a short sale," says Beverley Hourlier, a real estate agent in San Diego. Pre-foreclosure doesn't necessarily mean that the homeowner is underwater, and it doesn't guarantee that the home will be foreclosed on. In fact, says Field, if homeowners facing pre-foreclosure contact their bank, they have a chance of saving their home. "The bank doesn't want the property back," she says. "They want you to be able to save it, but you have to take action. Don't bury your head in the sand and stop opening the mail. Contact your bank right away, and they may be able to find a way to work with you," Hourlier adds. Foreclosure Foreclosure means the property lender has taken back the property for lack of payment. It's a process," says Tracey Martin, a real estate agent in Salinas, CA. Buying a foreclosure is completely different from a typical home purchase. Generally, foreclosures are bought at auction sight unseen, meaning you could end up with a home in need of serious repairs. "You don't have investigatory rights; you're buying a property as is," says Field. Field also explains that experienced investors go into foreclosure auctions with cash and a formula. "For someone who just wants to buy a home to live in, it's not a smart idea," she says. But whether you're a seasoned pro or a first-time home buyer, a foreclosure can be a risky investment for anyone. Many foreclosure homes are still occupied by their former owners, whom you would be responsible for evicting. Furthermore, "if you buy, you assume all liens, IRS liens, and other mortgages possibly tied to the property," says Kevin Sucher, a real estate agent in Portland, OR. Before signing on the dotted line, do as much research about the property as possible and be prepared for surprises. Field suggests investigating websites that sell foreclosures, as they tend to have more guidance for the novice than an auctioneer at the courthouse steps. Also, when bidding on foreclosed homes, be aware that having the highest offer won't necessarily nab you the property. "Servicers will go with the buyer most likely to close. They may take a lower price from someone with better terms," Field explains. In short, unless you're shopping with cash, you might have to bid on several properties before you find a winner. "It can be done," Field says, "but it requires caution, patience, and ideally guidance from someone with experience buying foreclosures." Article Written By: Audrey Ference has written for The Billfold, The Hairpin, The Toast, Slate, Salon, and others. She lives in Austin, TX. Follow @audreyference  Marie Kondo, the internationally famous personal organizer, author and host of the Netflix reality series "Tidying Up With Marie Kondo" has ticked off all the bookworms on Twitter. In her book "The Life-Changing Magic of Tidying Up," she suggests that she tries to keep her personal book collection down to about 30 volumes. The entire internet recently took issue with this and shouted into The Void that Marie Kondo could rip the contents of their overstuffed bookshelves from their rigor mortis-stiffened fingers.

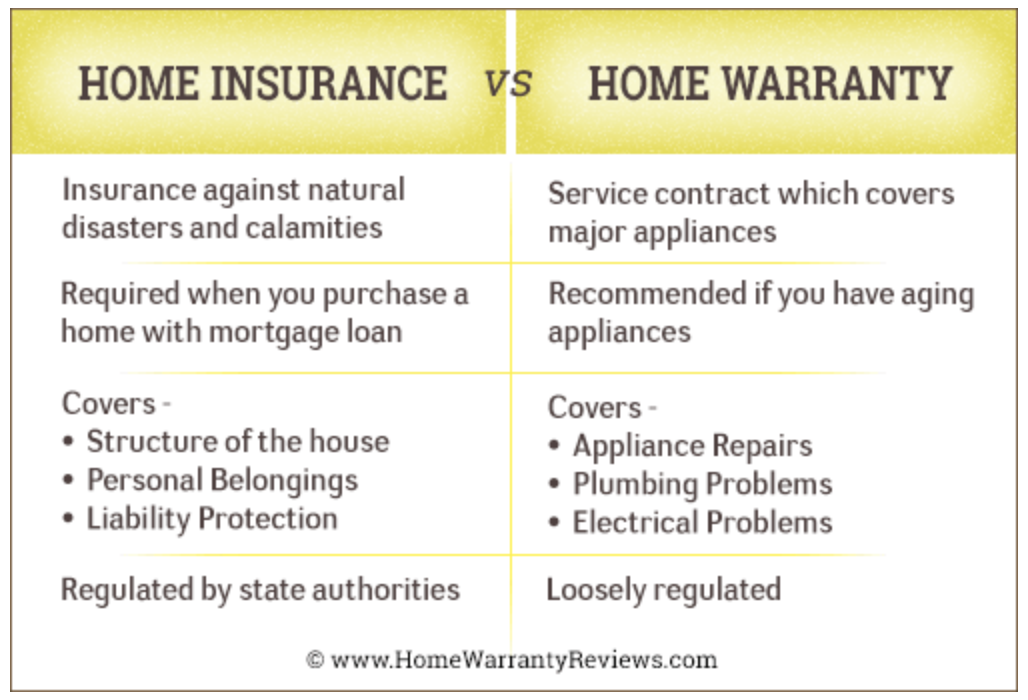

From this, we are to understand that many people feel a passionate attachment to, not only their books, but their belongings in general. But is living up to our necks in stuff good for us? Cluttered Life, Cluttered Mind"Remember the Zen proverb: The way a man does one thing is how he does everything," says Regina Leeds who has been a personal organizer for over 30 years and has authored 10 books on organizing and decluttering, including "One Year to an Organized Life: From Your Closets to Your Finances, the Week-by-Week Guide to Getting Completely Organized for Good". "Chaos in physical space means chaos in one's mind." And, sure, somebody who makes their living helping people organize their lives would certainly tell you it's unhealthy to live in a mouldering canyon of your own possessions, but the research also suggests living in a disorderly or cluttered space definitely affects our mental health. Of course, hoarding, the compulsive acquisition of new things and inability to get rid of any of them, points to a more severe mental health disorder, but research shows living in a house where things casually pile up to the point where you're navigating bedside tables teetering with towers of paperbacks and kitchen tables covered with two weeks worth of junk mail can wreak its own kind of havoc on your life. The Cortisol ConnectionThe reason living in a messy environment can cause emotional distress has a lot to do with our visual field and what we can mentally and physically keep up with. A nice, neat living space feels good, partly because there's less to look at -- there's less for the brain to do in an uncluttered space. This helps us focus on the task at hand: One 2011 study published in the Journal of Neuroscience found that study participants were more productive and less irritable if their workspace was clear of visible clutter. This is because an overwhelmed brain makes the stress hormone cortisol, which is great for helping you run away from a swarm of angry bees, but it's not helpful when you're hanging out all day at work, steeping in low levels of cortisol. Living on a constant cortisol drip can lead to anxiety, depression and other mental health problems like post-traumatic stress disorder. Research shows that women's cortisol levels are affected by a messy living situation more than men's. Two studies published in 2010 in the Journal of Personality and Social Psychology and conducted by a team of researchers at the University of Southern California found that, among 30 two-income couples with school-aged children living in the Los Angeles area, the woman in the relationship was more likely to take the psychological hit from a messy house. In the first study, wives were the ones who experienced elevated cortisol levels throughout the day as a result of a cluttered living space, and because they were more likely to be responsible for household chores, their stress hormones remained high after they got home. ProcrastinationOne study published in the June, 2018 issue of Current Psychology finds that people who live in cluttered spaces are more likely to procrastinate than those who don't. Procrastination itself isn't necessarily harmful, but it can lead to bad outcomes like poor performance at school or work, high anxiety or depression, and the loss of belief in your own ability to get anything done. For this study, the research team asked groups of people of different ages (college students, adults in their 20s and 30s, and older adults with a mean age in the mid-50s) how cluttered their spaces were and how much they found themselves procrastinating in their daily lives with everyday tasks like paying bills or doing laundry. The study found a strong link between clutter and procrastination in participants of all ages, but the vexation associated with it was more pronounced in the older groups. How to Get OrganizedIn many affluent countries, the clutter problem comes from simply having too much stuff, and many professional organizers counsel that getting rid of unnecessary belongings and keeping them out of the house is key. There are about as many methods to decluttering your living or working space as there are spaces to declutter, but Leeds suggests we take it easy on ourselves and realize organization is a learned skill we can practice. "A person who grew up in a household without an organized parent may feel shame that his or her environment as an adult is in chaos, rather than simply realizing that organizing is a skill and they can learn how," she says. "Organizing is a life skill that has everyday application. We learn it initially and practice in our physical environments, but it has no limits." Article Written By: BY JESSLYN SHIELDS for Howstuffworks.com  Ever wondered what is the difference between a home warranty and homeowners insurance? Are they not the same? Let’s find answers to these questions.

While home warranty and home insurance products may come across as same, they are totally different. The coverage, cost, terms, and conditions vary greatly. Home insurance is compulsory in some cases whereas home warranty is a recommended choice. DIFFERENCE BETWEEN HOMEOWNERS INSURANCE VS HOME WARRANTY INSURANCE Now that you have a fair idea of the difference between home warranty vs home insurance, let’s summarize. First, figure out what is the homeowner’s insurance coverage for appliances. A home warranty offers protection for your major appliances, as well as plumbing and electrical units. It covers the cost of repairing or replacing major household appliances in case they break down. This is provided they meet the terms and conditions of the home service contract. Home insurance covers your home in the event of damage due to natural calamity or man-made disasters. It offers you protection from lawsuits in case of third party involvement. For example: If your neighbor visited you, fell by accident and got injured. If he decides to sue you, then home insurance will take care of the claims. Home insurance is mandatory if you have a mortgage on your home. WHAT DOES A HOME WARRANTY CONTRACT COVER?Items covered by a home warranty may vary by company and plan, but typically homeowners insurance that covers appliances include:

Liability insurance will protect you from lawsuits in the event that someone is injured on your property. Home insurance will only ensure your personal items in case they are stolen or ruined in a disaster. Repairs and replacements due to wear and tear are not covered. WHAT DOES A HOME INSURANCE POLICY COVER?The insurance policy varies depending on your state of residence and type of policy, but generally, it will cover the following.

Home sellers typically pick up the tab for the first year of coverage. Extended coverage plans for pools, spas and washers and dryers can be purchased at an extra cost. Insurance cost varies from state to state and depends on the extent of coverage and the location of the property. But standard insurance can cost any homeowners insurance is between $300 and $1,000. HOW TO CHOOSE A HOME WARRANTY?When you are planning to buy a home warranty, make sure that you do some research. Check our home warranty reviews section that provides pricing, comparison, quotes and consumer reviews of all major companies. When you are getting price quotes, inquire to look over a sample policy. Bear in mind to understand the entire policy, together with the fine print. Another advantage of a home warranty policy is that it is transferable. The home warranty is passed on to the new owner. This has proved to be a well-liked feature amongst home buyers. Homes with home warranties are selling at increased prices and in much shorter times. This in itself could make it sensible to get a home warranty policy. HOW TO MAKE A CLAIM?When a covered appliance breaks down you need to contact your warranty company. A warranty company already has business ties with different service vendors. They will, in turn, contact a service repairman to come to your home and repair the appliance. The repairman will fix the item or recommend replacing it. The service repairman will bill your warranty company directly. But you have to pay a service charge when the repair person visits your home. HOW TO CHOOSE HOME INSURANCE?With any kind of insurance, it is always a good idea to shop around. You should evaluate benefits and prices as most insurance companies will provide you with a policy discount. Ensure you read the policy before writing a check and ask any queries that you have in mind. So, the conclusion is that home warranty and insurance are complementary to each other. You can choose to protect everything you own, provided you can afford to. Keep in mind that these insurance products do cost a bit more. But compared to the benefits and the peace of mind you get, it seems like a very small amount. Ensure your home as well as buy a home warranty all within your budget. Do I Need A Home Warranty When Buying A House?Yes, you should have a home warranty when buying a condo or a house. Usually, the sellers include a home warranty as part of the sale. A home warranty covers appliances and systems like air conditioning, plumbing, dishwasher and is responsible for items in the condo. Do You Really Need Homeowners Insurance?Homeowner’s insurance covers damage due to fire, theft and natural disaster. While a home warranty covers damage due to wear and tear. Based on where you live, you should purchase additional coverage for insurance. This is because earthquakes and floods as most events are not covered in the basic plan. What Does A $500 Home Warranty Cover?A standard home warranty would cost around $350 to $500 a year or more. This is based on the type of home warranty company and the plan. This warranty typically covers water heater, electrical systems, sump pump, exhaust fans, kitchen appliances, exhaust fans, and ceilings. Should I Get Homeowners Insurance?Homeowners insurance will ensure that your home is covered from natural disasters and theft. If you mortgage your home then your lenders would expect you to have home insurance. This will protect your home from unforeseen circumstances. |